Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, fell 2% for the week.

- Equity market investors in Europe are depressed. Is there a potential bull case for European stocks?

One of the more notable market developments since the election has been the sliding of Europe’s stock markets. The US market’s S&P 500 index has risen 2% since election day, whereas a basket of European stocks tracked by the Vanguard FTSE Europe ETF has slipped 4%.

Through the better part of the first half of 2024, the US and Europe had similar returns. However, Europe’s stock markets have fallen 9.7% since October 1st.

Perhaps October was the inflection point when investors began pricing in an increased probability of a Trump victory. The market’s consensus is that a Trump administration will be negative for European markets, as the Trump administration is viewed as more combative on trade and less likely to support defense spending in the region.

Economist Dario Perkins of London-based TS Lombard noted this week that since the election, investors have built in rather catastrophic expectations for Europe. He observed that everyone in European markets is, simply put, depressed.

He then performed a quick analysis of possible positive factors that are incongruous with these currently dreadful market expectations:

- Real incomes in Europe are growing;

- European Central Bank monetary policy is easing;

- The so-called “Trump Crisis” for Europe may force higher defense spending in the region;

- There is potential for more coordination and focusing of European minds on investment in the region;

- Economic performance in the “peripheral” economies has been well above expectations.

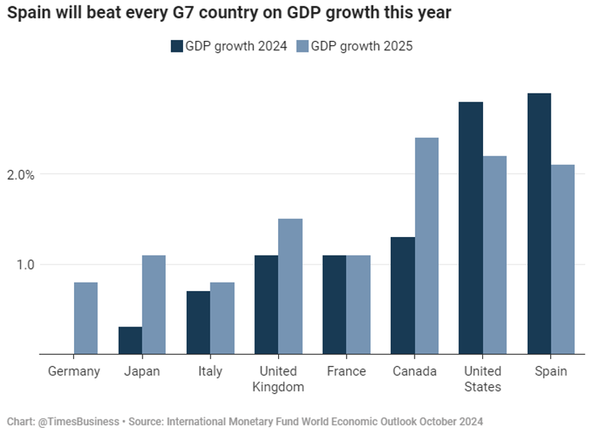

Regarding the last bullet point, the Times of London reported this week that the Spanish economy is one of the fastest growing in the developed world, ahead of the US:

Like Mr. Perkins, Jon Sindreau, economics journalist at the Wall Street Journal, believes that the long-term bull case for European equities is that Trump 2.0 will be a catalyst for regional transformation. He notes that shares in European defense contractors such as BAE Systems, Rheinmetall, and Thales have jumped since the election. Longer-term, the EU wants members to direct more than 50% of their spending to European contractors.

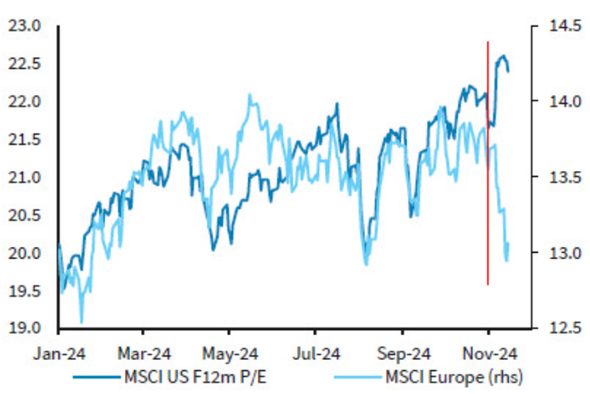

Also, equity valuations in Europe are reasonable. Versus the US market, Europe is outright cheap. Investors have set a low bar for European stocks – they trade at a P/E of 13x versus the US market’s 22x P/E, a 40% discount that widened substantially post-election (per chart below). It would not take much of a positive economic surprise in Europe for decent returns there.

Source: IBES, Barclays Research, November 2024

Editor’s comment: Our weekly note will resume in December. We wish all our clients, partners in our communities, and professional colleagues a safe and happy Thanksgiving!

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2024.