Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 4.7% for the week.

- The wide consensus is that long-term interest rates will rise in the second Trump administration. There are reasons to reconsider this outlook.

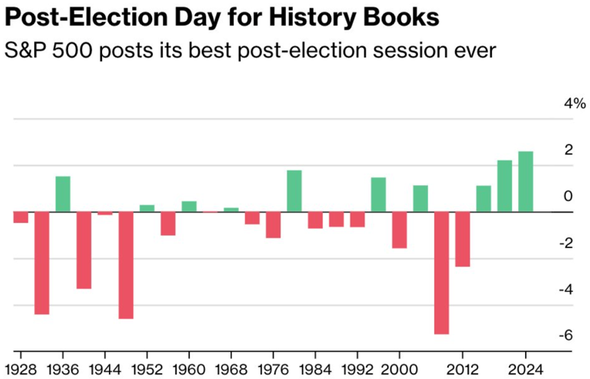

The US stock market posted its best post-election day ever after Trump’s election win this week, rising 2.5%. The previous best post-election day was the trading session following Biden’s election in 2020, when the market rose 2.2%, as reflected in the chart below:

Source: Bloomberg, November 7, 2024

Per usual, the stock market dominated headlines in the financial press. Lost in the shuffle were a few peculiar shifts in long-term interest rates. The overwhelming consensus across economists and anyone who writes about capital markets is that the Trump economic agenda will create real economic growth and structurally higher inflation, all of which will result in persistently elevated interest rates.

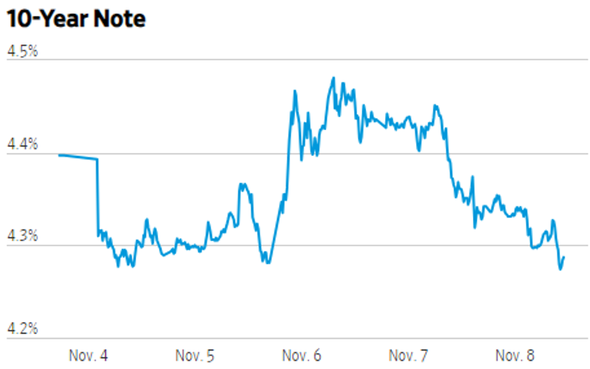

The 10-year US Treasury note yield is the bellwether long-term interest rate for markets. The yield on the 10-year note spiked on Wednesday following the election, rising from 4.3% to almost 4.5%. By the end of Friday, however, the yield had fallen to a hair below where it started the week:

Source: Wall Street Journal, November 8, 2024

The Federal Reserve met on Thursday (it was a busy week!) and decided to lower its target interest rate by 0.25%. Jerome Powell, the Fed chairman, was dovish on inflation at his press conference following the Fed’s meeting. His optimism on continuing disinflation and the Fed’s decision may have guided yields down from the Wednesday peaks.

That rate cut was no surprise, however, so perhaps there is more to the story. In a note this week, Matthew Klein made an out-of-consensus observation about the potential for lower interest rates in the future.

It begins with the simple premise that Americans hate inflation. It may not be a stretch to posit that if there is a tradeoff between high inflation, felt by everyone, and high unemployment, felt by a smaller group of people, that the electorate may prefer high unemployment.

The tradeoff between inflation and employment is far from established economic science, but the idea carries larger political considerations. One likely factor (amongst many) playing a part in the election outcome this week was the high inflation felt by voters over a relatively short period, in 2022 and 2023. If voters believe that the post-COVID government stimulus was primarily responsible for the inflation (a debate topic for decades to come), perhaps there will be less political support for fiscal stimulus in the future to meet economic downturns. Mr. Klein argues that less fiscal stimulus in the face of recessions could result in longer downturns and thus, eventually, lower interest rates.

There are other long-term reasons to believe that interest rates will not go higher, such as the advent of AI and automation. One week’s ticks upward and downward in the 10-year Treasury note are hardly proof of anything, but there are reasons to treat the nearly unanimously held high-interest rate outlook with some skepticism.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication.

Copyright Indiana Trust Wealth Management 2024.