Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, fell 1.4% for the week.

- Investors should be skeptical of narratives about how next week’s presidential election will shape capital markets in the years to come.

Last week, JP Morgan suggested that the recent rise in long-term interest rates could be linked to the possibility of a Trump election victory next week. A popular bond market “Trump Trade” has been to wager that short-term rates will fall whilst long-term rates will rise – a yield curve “steepening” trade.

Why would long-term interest rates be higher in the future in a Trump presidency? Mainly, JP Morgan suggests, it would be the outcome of federal budget deficit-fueled economic growth. The Committee for a Responsible Federal Budget estimates that Trump’s policies would increase federal debt by $7.75 trillion over the next decade.

However, as James van Geelen from Citrini Research noted on Wednesday, there are more concrete reasons to explain the shifting yield curve. Those include ongoing disinflation, stabilizing employment, and economic growth. Also, that same Committee projects that Harris’s policies will increase the debt by $3.95 trillion, a nontrivial figure. If future deficits matter, then rates are rising because of either election outcome.

Narratives for how elections will impact markets usually rely upon political clichés. Some of these clichés are born from campaign promises, and – now bear with me here – politicians often do not keep those promises.

One such narrative can be seen in stocks that could be impacted by Trump’s proposed tariffs on Chinese imports. Mr. van Geelan notes that the market is already pushing up stock prices on companies with a lower percentage of products from China (Ollie, Arhaus, and BJ’s) versus those with higher Chinese imports (Five Below, Restoration Hardware, Wayfair, and Target).

If those tariffs do not materialize, then these trades won’t work very well. Who knows what the trade outcomes would be under a Trump administration? Once the election is over and reality sets in, it is likely that most of these trades tied to political narratives will unravel.

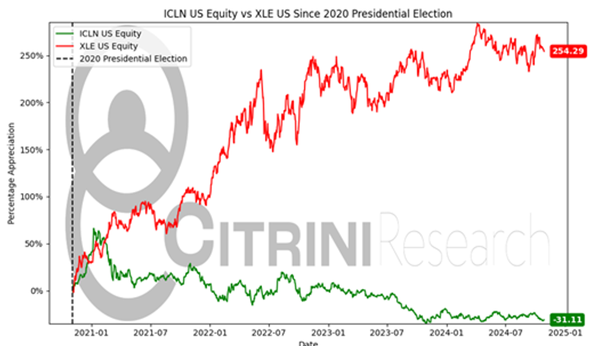

Mr. van Geelan points out that one needn’t go back too far in history to find a salient example of how pre-election market narratives can be quickly obliterated. When Biden was elected in 2020, a popular cliché-based trade was to bet on “Democrat” clean energy stocks such as First Solar and Vestas Wind Systems while betting against “Republican” fossil fuel names such as ExxonMobil and Chevron.

Subsequently, US oil production reached all-time highs. Below is a chart of a basket of “fossil fuel” stocks (“XLE”) and a basket of “clean energy” names (“ICLN”) since the 2020 election:

Source: Citrini Research, Bloomberg “Odd Lots”, October 30, 2024

From Biden’s election win to date, fossil fuel stocks are up a cumulative 255%. Clean energy stocks are down 31%.

Elections are personal. Emotions are running high. This can cloud objective thinking and can make investors susceptible to easy market narratives that fit their political beliefs, when the reality is that how elections impact capital markets is unpredictable.

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication.

Copyright Indiana Trust Wealth Management 2024.