Indiana Trust Wealth Management

Investment Advisory Services

by Clayton T. Bill, CFA

Vice President, Director of Investment Advisory Services

- The U.S. equity market, represented by the S&P 500 index, rose 0.9% for the week.

- As a result of their explosive performance in recent years, the US technology and communications services sectors now represent a large weight in the US stock market and, by extension, the global stock market. Have tech stocks become overvalued?

As measured by the index provider MSCI, the US currently makes up 64% of the global stock market. Ten years ago, the US share was less than half. The increase in the US weight is attributable to relative performance: the US stock market has trounced stock markets around the world over that time.

The key drivers for US outperformance have been the technology and communication services sectors, which combined make up over 40% of the US stock market. Investor enthusiasm for AI’s expected impact on semiconductor and cloud spending is chiefly responsible for the bounce in technology shares in recent years.

The rise in US tech stock prices has also stretched valuations for the sector. On a price-to-sales basis, the tech sector is as richly valued as it was back in 2000 during the dot-com bubble. That episode did not end particularly well for tech stock investors, although patient, diversified investors recovered and have flourished since.

There are a few key differences between the current environment and the dot-com era. First, the big tech and communications names such as Nvidia and Meta generate large profits and free cash flows, unlike the many speculative and unprofitable high-flying internet stocks from 25 years ago. Nvidia’s gross profit margin has soared since the start of the AI investment cycle and stands at 75%. Perhaps a higher-than-normal price-to-sales valuation should be expected.

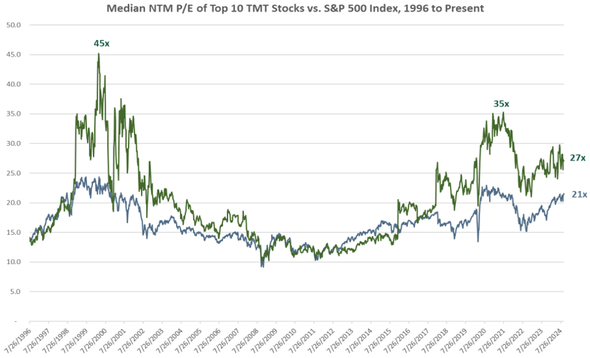

Also, when gauged by price-to-earnings (P/E) ratios, big tech names are more expensive than the overall US market – but are nowhere near the high valuations reached back in 2000. The chart below shows the median P/E for the top ten US technology stocks (green line) versus the overall S&P 500 (blue line), back to the late 1990’s. Tech stock valuations (27x) are higher than the overall market (21x) but are still quite a distance from what tech expanded to at the turn of the millennium (45x).

Source: Deb Koch, CFA, Senior Equity Analyst, Technology. Northern Trust Asset Management, October 2024

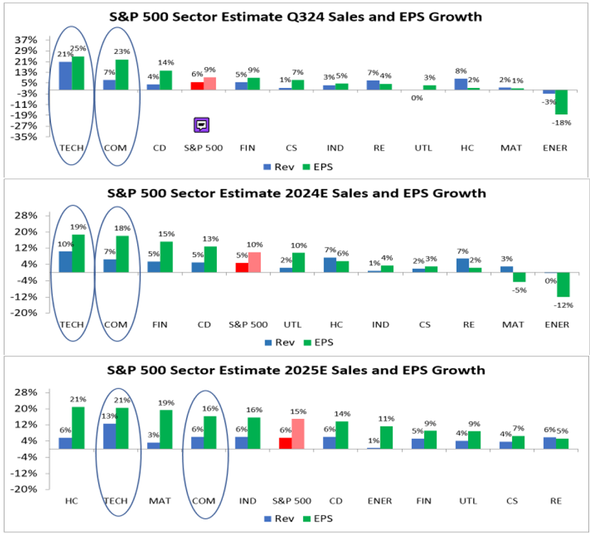

Earnings- and sales-based valuations are also baking in strong growth in tech and communications stocks over the next year. Those sectors, circled on the chart below, are expected to post strong results for 2024 and 2025.

Source: Deb Koch, CFA, Senior Equity Analyst, Technology. Northern Trust Asset Management, October 2024

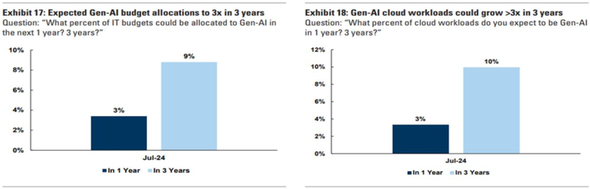

Whether the current valuations attached to next year’s tech earnings or sales are “too expensive” will depend on the direction of AI over the next several years. It is still early in the generative AI spending ramp-up to say whether those stocks are overvalued or who the ultimate winners will be. A recent Goldman Sachs survey of Chief Information Officers (see below) reflects expectations for a massive shift in IT budgets to support generative AI and cloud workloads over the next three years. Investors have taken note.

Source: Goldman Sachs Global Investment Research, October 2024

__________

IMPORTANT DISCLOSURES: All info contained herein is solely for general informational purposes. It does not take into account all the circumstances of each investor and is not to be construed as legal, accounting, investment, or other professional advice. The author(s) and publisher, accordingly, assume no liability whatsoever in connection with the use of this material or action taken in reliance thereon. All reasonable efforts have been made to ensure this material is correct at the time of publication. Copyright Indiana Trust Wealth Management 2024.